")

______________________________________________________

Lira Crashes To All Time Low After Turkey Shocks With 200bps Rate Cut Despite Soaring Inflation

BY TYLER DURDEN

THURSDAY, OCT 21, 2021 – 07:26 AM

To be fair, the writing has been on the wall for the past three years, ever since Turkey’s authoritarian ruler and de facto central bank head Erdogan started firing Central Bank governors any time they refused to cut rates to fight inflation in compliance with Erdoganomic, a reminder of which we got just last week when Erdogan fired three more Turkish central bankers, sending the lira plunging…

… in a move which we suggested that one way or another, Erdogan wants hyperinflation, and currency collapse.

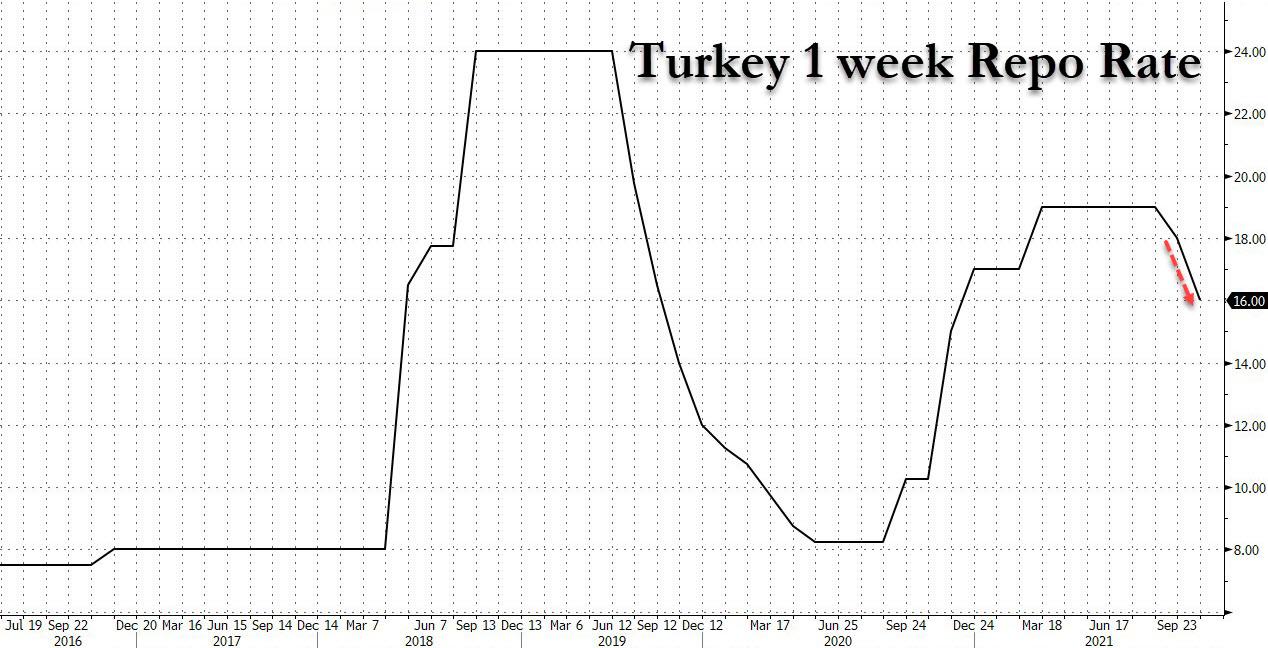

So fast forward to this morning when central bankers, knowing they would lose their jobs if they didn’t slash rate by even more than the market expected (and the market expected a generous 50-100bps) cut despite the highest inflation in over two years (the latest CPI print came in at 19.58%), had no choice but to slash and they did just that and Turkey’s Central Bank cut its one-week repo rate by 200bps, from 18% to 16%, double what consensus expected (15 of 26 economists in Bloomberg’s survey expected 17.00%, with the rest expecting a 50bps cut), arguing inflation is “transitory” if adding that it has limited room left for further reductions this year (actually no, it will keep cutting because that’s what Erdogan wants).

The “recent increase in inflation has been driven by supply side factors,” the central bank said, calling them transitory. “The Committee assessed that, till the end of the year, supply side transitory factors leave limited room for the downward adjustment to the policy rate.”

Putting the rate cut in its (hyperinflationary) context, the rate cut virtually guarantees that Turkish inflation is about to turn even more hyper :

Advertisement

______________________________________________________

In a hilarious twist, the TCMB justifed this insane move by pointing the finger to “advanced economy” central banks and arguing that since they see inflation as temporary – and since the Fed continues to inject hundreds of billions of liquidity every month – surely inflation must be transitory, and so Turkey can surely afford a rate cut, to wit:

Central banks in advanced economies assess that the rise in inflation would be mostly temporary along with normalization in demand composition, easing of supply constraints and waning base effects. Accordingly, central banks in advanced economies continue their supportive monetary stances and asset purchase programs

Recent increase in inflation has been driven by supply side factors such as rise in food and import prices, especially in energy, and supply constraints, increase in administered prices and demand developments due to the reopening. It is assessed that these effects are due to transitory factors

All one can do here is laugh. Anyway, here are some more “explanations” for the shocking cut:

Despite the recovery in global economic activity in the first half of the year, recently published confidence indices have started to decline due to the effect of the pandemic….

The MPC assesses that, until the end of the year, supply-side transitory factors leave limited room for the downward adjustment to the policy rate.

Advertisement

______________________________________________________

Leading indicators show that domestic economic activity remains strong, with the help of robust external demand… Improvement in annualized current account is expected to continue in the rest of the year.

Meanwhile, the “tightness in monetary stance has started to have a higher than envisaged contractionary effect on commercial loans. Strengthened macroprudential policy framework has started to curb personal loan growth.” Or said otherwise, if we don’t cut, the big bogg will fire us all.

In parting, the TCMB said that the “Bank will continue to use decisively all available instruments until strong indicators point to a permanent fall in inflation and the medium-term 5% target is achieved.”

Not surprisingly, now that it is abundantly clear that Erdogan will s*******e the lira before he admits he has been wrong all along, the TRY crashed to a new all time low, plunging as much as 2.9% to just shy of 9.50 vs the USD, a move which we are confident will only accelerate to the downside with Erdogan having openly invited hyperinflation, and only a popular uprising having some chance of halting this catastrophic turn of events, yet a revolution will hardly be lira positive and as such expect much, much more weakness in the now doomed currency.

The cut “can be interpreted as a very strong message to market participants that the central bank intends to ease monetary policy regardless of negative consequences of the precipitous fall in the value of the lira,” said Piotr Matys, a senior currency analyst at InTouch Capital in London, echoing what we said one week ago.

“Today’s decision is an obvious disregard of warnings the market has already sent the CBRT that lowering rates – when inflation is close to 20% and core inflation cannot be used as a valid argument to cut rates – is a policy mistake,” Matys said, referring to the central bank by its English-language acronym.

Erdogan’s central bank puppet, Kavcioglu will update the bank’s base-case scenario for inflation through the rest of 2021 and the following two years on Oct. 28, and answer questions from economists and reporters. The central bank currently sees consumer-price growth finishing the year at 14.1%, a more optimistic forecast than the government’s latest estimate of 16.2%. In reality, expect hyperinflation.

Source: Zero Hedge

______________________________________________________

If you wish to contact the author of a post, you can send us an email at voyagesoflight@gmail.com and we’ll forward your request to the author (if available). If you have any questions about a post or the website, you may also forward your questions and concerns to the same email address.

______________________________________________________

All articles, videos, and images posted on Dinar Chronicles were submitted by readers and/or handpicked by the site itself for informational and/or entertainment purposes.

Dinar Chronicles is an informational news aggregator. All content, including third-party reports and community commentary, is provided for educational purposes only. We do not provide financial, legal, or tax advice. We do not recommend the purchase or sale of any currency or investment. Please consult with a licensed professional before making any financial decisions.

Copyright © Dinar Chronicles

Advertisement

______________________________________________________

______________________________________________________

7-25-26")

{kind=link}

{kind=link}

{kind=link}

{kind=link}