______________________________________________________

Europe Has Been Preparing a Global Gold Standard Since the 1970s: Part 2

BY TYLER DURDEN

MONDAY, OCT 17, 2022 – 03:30 AM

By Jan Nieuwenhuijs of GainesvilleCoins.com

There is more evidence of how European central banks are equalizing their monetary gold reserves proportionally to Gross Domestic Product (GDP). Secret agreements make countries sell or buy gold to balance gold reserves within Europe, and relative to large economies abroad. Evenly distributed gold reserves are a requirement for a stable transition towards a gold standard whereby concurrently the debt overhang can be extinguished. Europe has been preparing for this reset.

If you haven’t read part one recently, please read the summary below.

Recap of Part 1

After Nixon unilaterally suspended the last vestige of the gold standard in 1971, Europe was not amused. Led by France, which wanted to return to a gold standard, the Europeans began countering dollar dominance and slowly prepare a new arrangement. In 1973 the European Economic Community (ECC) publicly stated in the New York Times: “[Europe] will promote agreement on international monetary reform to achieve an equitable and durable system taking into account the interests of the developing countries.” Clearly, Europe didn’t envisage a dollar standard for the long haul, as it isn’t equitable nor durable.

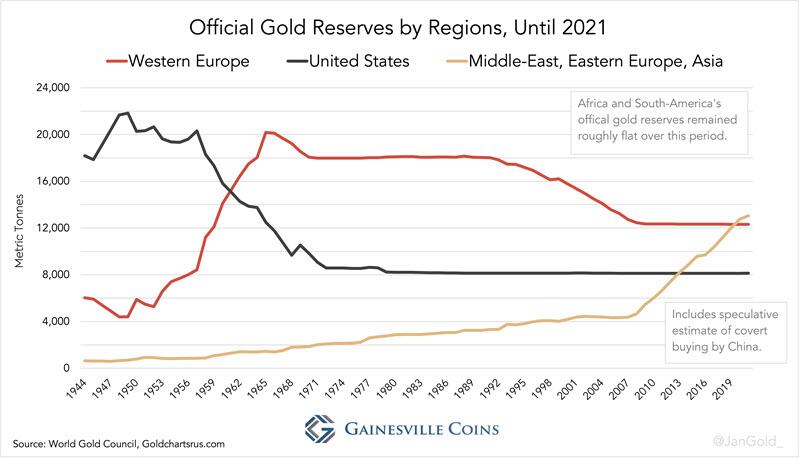

Since the 1960s Europe was holding most of the world’s monetary gold. In the 1990s several Western European central banks started selling gold to equalize their gold reserves among each other and large economies outside Europe. From 1999 until 2008 they did so officially through a “concerted programme of sales” dubbed the Central Bank Gold Agreements (CBGA).

Advertisement

______________________________________________________

In 2011, the Minister of Finance of the Netherlands was asked in parliament, where he had to speak the truth, for the main reason why the Dutch central bank (DNB) had sold 1,100 tonnes of gold since 1993. His answer:

Through gold sales in the past, DNB brought its relative gold holdings more in line with other important gold holding nations. … At the time it was established that DNB held a relatively large amount of gold internationally.

Another question directed at de Jager was if he could confirm if other nations were increasing their official gold reserves in the past years. His answer:

The buyers are developing nations whose international reserves are growing, or historically have a small gold stock.

After 2008, European central banks began radically changing their communication about gold. The Bank of Italy states on its website that “gold is an excellent hedge against adversity,” and “unlike foreign currencies, gold cannot depreciate or be devalued.” The Dutch central bank stated, “Gold is the perfect piggy bank,” and, “if the system collapses, the gold stock can serve as a basis to build it up again.”

Advertisement

______________________________________________________

The fact that several European central banks (The Netherlands, Austria, France, Germany, Hungary, Poland) repatriated gold in recent years signals they carefully evaluate cost efficiency, security, and liquidity of their monetary precious metal.

Upgrading all gold reserves to current wholesale industry standards—in example done by France, Sweden, and Germany after 2008—is another indicator of European central banks preparing for a gold standard. Any bars that don’t adhere to the LBMA Good Delivery standard aren’t liquid in international markets.

Comments by ex-high ranking officials may be connected to a gold overhaul of the international monetary system. Jean-Claude Trichet, former President of the European Central Bank, stated in 2014: “The global economy and global finance is at a turning point, … new rules have been discussed not only inside the advanced economies, but with all emerging economies, including the most important emerging economies, namely, China.”

Why Equalize Gold Reserves?

Gold reserves evenly spread across nations, proportionally to their GDP, allows a smooth transition towards a global gold standard. In 1971, Europe was holding the largest share of the world’s gold reserves. What is now the eurozone was then holding 45% of all monetary gold, while contributing for 24% to world GDP. Switching to a global gold standard with such imbalances would have pushed the world into steep deflation. To illustrate, countries that owned zero or too little gold relative to GDP, as many developing nations did at the time, would have to buy in to participate. Resulting in upward pressure on gold, which is deflationary when gold is the unit of account.

There were also other reasons for Europe not to switch to a gold standard at the time. The United States opposed going back to gold and it was defending Europe against the Soviets. Germany was threatened to be left to its own devices if it didn’t play along with the dollar standard. Europe decided to further unite, create an alternative to the dollar (the euro), and facilitate monetary gold to be spread more evenly globally.

European central bankers must have realized the inevitability of a debt spiral when the world went from a gold to a paper standard in 1971. Their preferred “equitable and durable” monetary reset would be international, depriving the U.S. of its exorbitant privilege, and extinguish the debt overhang created over time. One way of cancelling debt while still complying to the rules of economic scarcity is for central banks to buy up all excessive debt in the economy and then revalue gold. Unrealized gains on the liability side of central banks’ balance sheets, a produce of revaluing their gold, can then be used to cancel assets (bonds) on the asset side. These unrealized gains are recorded in a revaluation account, which can be seen as capital. Read this article for a more detailed description of revaluing gold to cancel debt.

Noteworthy is that European central banks were the first to value the gold on their balance sheets “mark-to-market” beginning in the late 1970s. The U.S. pressed for continuation of valuing monetary gold at its statutory price set under Bretton Woods, effectively trying to demonetize gold to protect the dollar hegemony. Until this day the U.S. records its gold reserves at a statutory price of $42.22 dollars per troy ounce.

When I asked the German central bank in 2021 if they considered revaluing gold to cancel debt, they replied: “we prefer not to speculate about any decisions … that might or might not be taken in the future.” So, instead of not responding or just say no, they communicated they don’t rule out this possibility.

Needless to say, if gold is evenly spread internationally all countries benefit to the same degree from the revaluation. Essentially, this is about the “international monetary reform to achieve an equitable and durable system taking into account the interests of the developing countries.”

More Evidence of the Eurozone’s Gold Balancing Project

There is an important statement on the website of the Austrian central bank (OeNB) about its aim to hold gold reserves as a percentage of GDP equal to its peers. From OeNB:

Advertisement

______________________________________________________

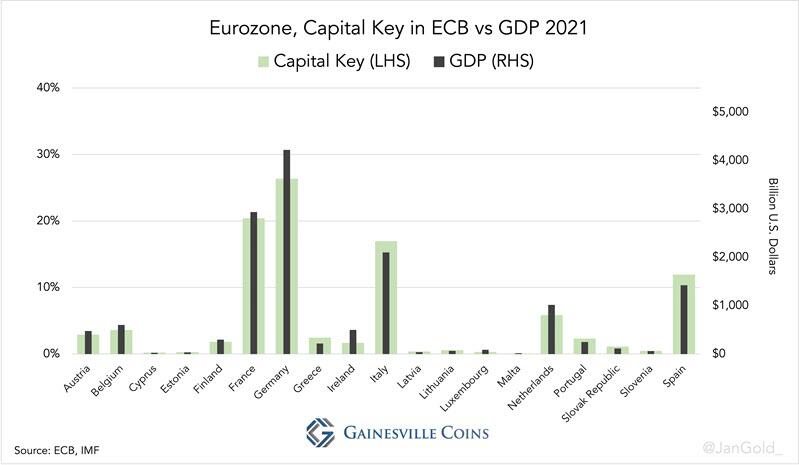

In terms of the Eurosystem’s overall gold reserves, OeNB’s current gold holdings roughly correspond to OeNB’s share of the ECB’s capital.

The Eurosystem consists of the European central bank (ECB) and all national central banks (NCBs) in the eurozone. NCBs own a share of the ECB based on their “capital key” that is calculated from a country’s GDP and population. The NCBs’ capital keys correspond to GDP, because population growth affects economic growth.

… the volume of gold held by OeNB is deemed to be appropriate relative to the size of both its total reserve assets and the Austrian economy [GDP].

Because nowadays eurozone NCBs rarely buy or sell gold, the above statement implies that during the selling period prior to 2008, countries in the eurozone pursued to equalize gold to GDP ratios. We don’t have to quibble whether this is fact or fiction. Once done, monetary and political policy is intended to produce the same growth levels throughout the eurozone, keeping gold to GDP ratios in line.

Not as explicit, though worth mentioning, is a statement from the French central bank:

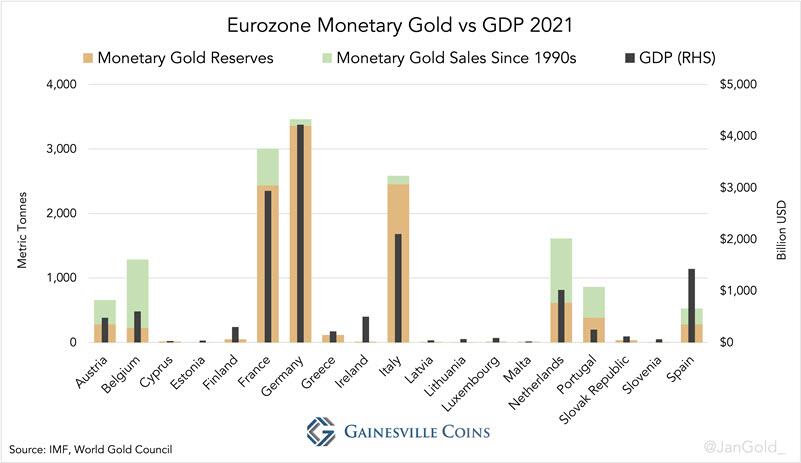

The Banque de France stores 2,435 tonnes of gold in its underground vault, situated 27 m below street level… These are France’s national gold reserves, valued at around EUR 80 billion.

France’s gross domestic product (GDP) or annual income is over EUR 2 trillion… The national gold reserves are thus equivalent to 4% of GDP…

The average (GDP weighted) gold to GDP ratio in the eurozone is 4%. France is on par.

Seemingly there are guidelines in the eurozone for NCBs to hold an appropriate amount of gold relative to GDP, but also relative to total international reserves, according to OeNB. Total international reserves comprise of gold, foreign exchange, and SDRs. OeNB’s quote regarding gold and total reserves can be linked to an old article by GoldCore about Belgium:

Advertisement

______________________________________________________

Belgium announced another sale of 203 tons of gold on March 27, 1996, stating that the sale had reduced the share of gold in total reserves to a level which would facilitate the National Bank of Belgium [NBB] in the process of European unification and which, corresponded to the proportion of gold in the total reserves of the Member States of the European Union.

There appear to be rules, adopted before the euro was launched in 1999, with respect to harmonizing gold to total reserves ratios. When I asked the Belgium central bank (NBB) if they could confirm they sold gold due to a requirement to be accepted into the eurozone, they replied:

The sales in question took place in the context of a more balanced composition of NBB’s reserves with regard to its integration into the European System of Central Banks, although it was not the result of a legal obligation.

Next, I asked what kind of agreement there was between European central banks, if not a legal obligation. NBB replied (emphasis and link added):

The aspects of management of international reserves that have not been communicated by NBB through its annual report(s) and/or press releases constitute confidential information that shall not be disclosed on grounds of professional secrecy laid down in Article 35 of the Statute of NBB, drafted February 22, 1998.

Unfortunately, it’s a secret. Of similar interest: when I was writing part one of this series, I asked an ex central banker in Europe if he was aware of a gold balancing policy during his tenure in the 1990s. “Yes,” he answered, “but I can’t talk about it; part of my duty of confidentiality.” The fact that so little is known about Europe’s balancing project, is because central bankers are not allowed to openly discuss it. OeNB is gently breaking the silence.

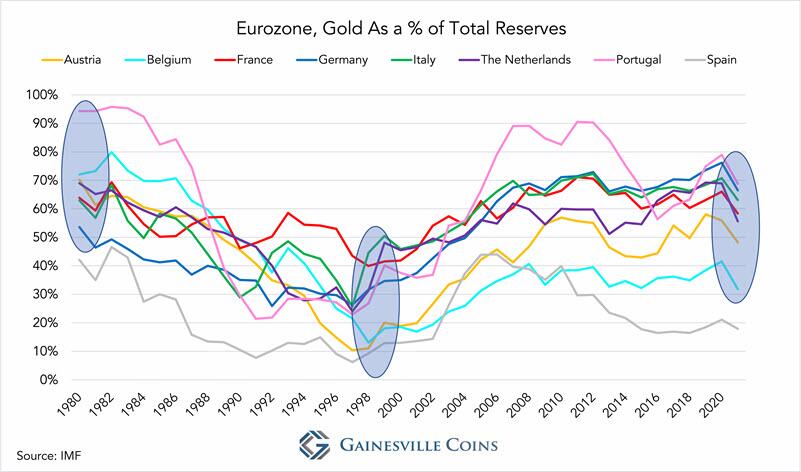

In lack of legal transparency, let’s turn to the data. Below is a chart showing medium and large eurozone countries’ gold share of total reserves from 1980 until 2021.

Aside from Spain, all medium and large economies’ gold to total reserves ratios were above 50% in 1980, below 50% in 1999, and are currently around 50%. Now consider that France, Germany, and Italy have hardly sold any gold during this period (chart 1). Austria, Belgium, The Netherlands, and Portugal, on the other hand, sold most of their gold while their ratios remained in the vicinity of their bigger peers. There must be a eurozone wide policy of coordinating international reserves to pull this off.

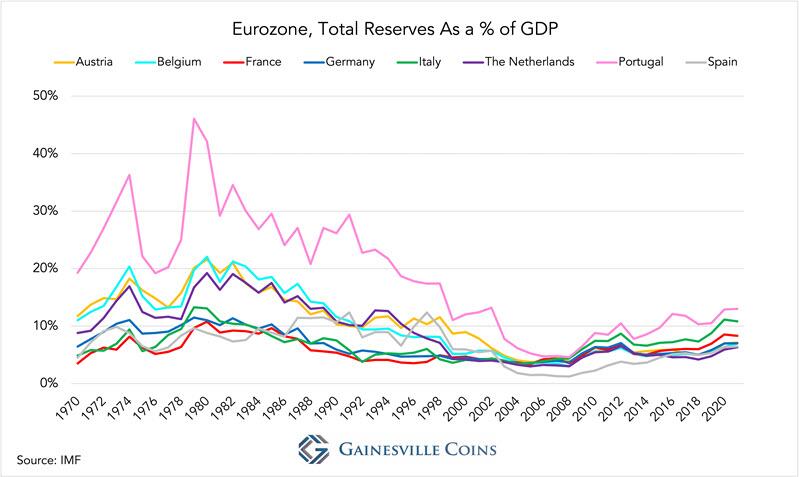

Crunching the numbers lead me to think that if gold to GDP and gold to total reserves ratios are matched, then total reserves to GDP ratios must be too. The data supports my hypothesis: the harmonization of total reserves to GDP ratios in the entire eurozone is indisputable.

Advertisement

______________________________________________________

As a gold analyst I will not pretend to be aware of every motivation for the eurozone’s efforts in harmonizing international reserves. What I do know is that measures are in place to be able to exactly equalize all gold to GDP ratios within the eurozone the minute before revaluing gold and resetting the monetary system.

It’s undoable for NCBs to precisely equalize their gold to GDP ratios every year. Some years country A will grow faster than B, which would make A have to buy gold or B sell. Given that gold is a politically sensitive asset, European central banks avoid adjusting their metal reserves periodically. It’s easier to ensure the medium and large economies are roughly on par in terms of gold to GDP ratios, then periodically equalize all NCBs’ total reserves to GDP ratios to be able to fine-tune gold imbalances when needed.

Some small economies have far too little gold. This isn’t a problem because these small imbalances can be fine-tuned within seconds. For example, Portugal sells a few tonnes to Malta (gold for dollars), France to Estonia, Italy to Spain, etc. The prerequisite for fine-tuning gold reserves is that all central banks have sufficient international reserves relative to GDP, which they do.

After putting everything together, I reckon the eurozone’s gold strategy is this:

- For the eurozone to own an adequate amount of monetary gold relative to economies outside of Europe based on GDP.

- To have roughly the same gold to GDP ratios in medium and large economies in the eurozone. This objective also serves the first objective.

- To have commensurate total reserves to GDP ratios in all countries in the eurozone to be able to fine-tune gold to GDP ratios before revaluing gold.

- To have approximately equal gold to total reserves ratios in medium and large economies in the eurozone. This objective is achieved by adjusting foreign exchange reserves and serves the previous three objectives.

- Stand ready for a monetary reset.

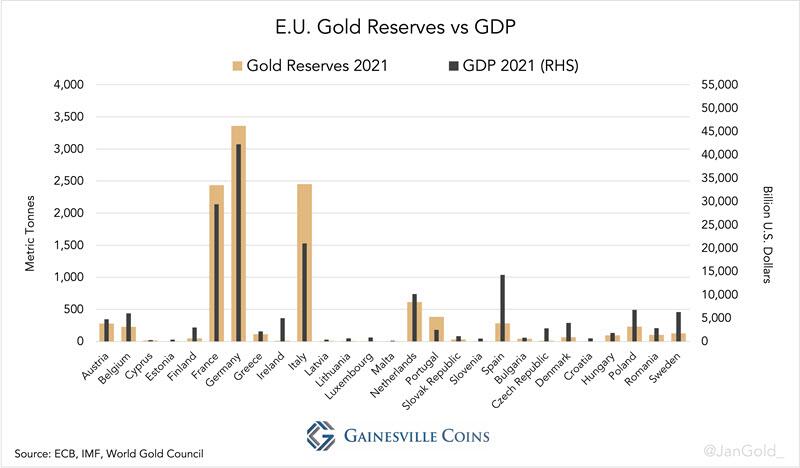

What About the Rest of the European Union?

The purpose of the European Union is that eventually all member states will adopt the euro—except for Denmark that has an opt-out. Below is an overview of all countries in the European Union and which of those are currently part of the eurozone. In the list the eurozone countries are blue, and “non-eurozone countries” are red.

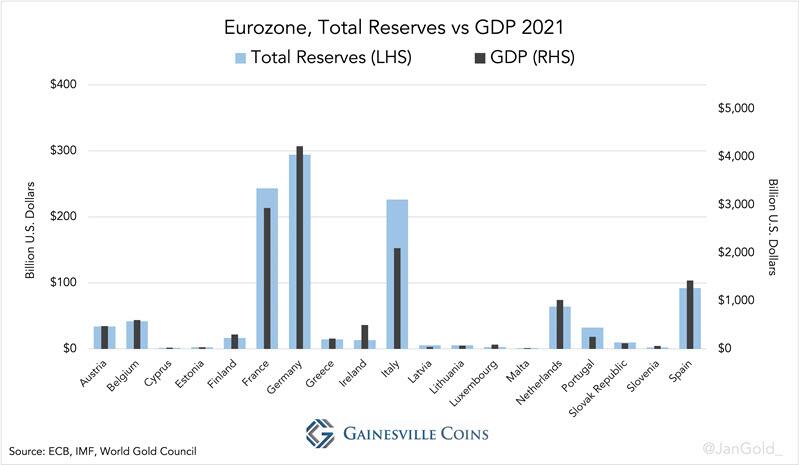

If countries like Belgium had to adjust the composition of their reserves before they were included into the Eurosystem in 1999, the non-eurozone countries have to do the same as we speak. To test whether this is true let’s have a look at a chart of European Union (E.U.) gold reserves versus GDP.

It’s not an immaculate fit, but it can’t be a coincidence that Hungary bought 91 tonnes of gold from 2018 until 2021 and is now on par with eurozone countries. Poland bought 99 tonnes in 2019, and has announced to buy another 100 tonnes in 2022, which will make it on par. The Czech Republic has announced to buy 90 tonnes in the near future, which will be a big start to bring it on par. These central banks may mention all sorts of reasons why they buy gold, one of them—equalize reserves—is concealed. In 2018, the central bank of Hungary disclosed it bought gold because “it may play a stabilising role … in times of structural changes in the international financial system.” As clear as can be when put in context.

For countries like Sweden and Denmark it’s more sensitive to buy gold, as they are part of the oldest advanced economies in the world.

According to my analysis the gold strategy of the eurozone and E.U. are one and the same. It’s mainly about medium and large economies having equal gold to GDP ratios, and all economies having equal international reserves relative to GDP. For non-eurozone countries the first requirement is nearly fulfilled, so let us examine the second.

Advertisement

______________________________________________________

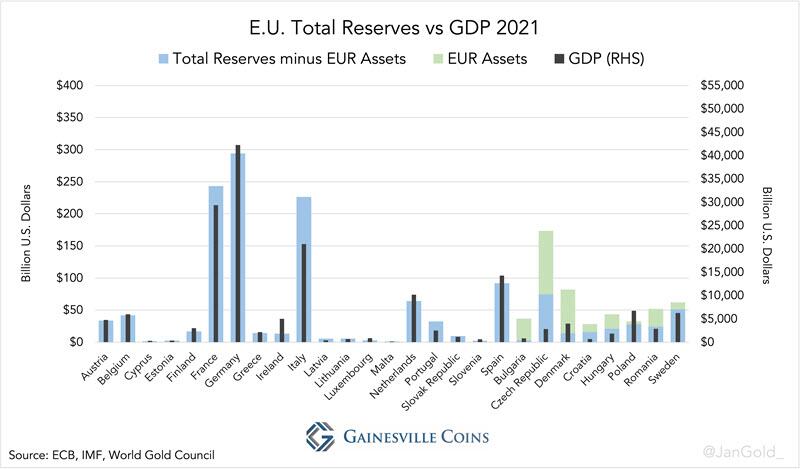

In the chart below I have plotted total reserves versus GDP for all countries in the European Union. For the non-eurozone countries I have subtracted euro assets from their total reserves, as these are currently part of their international reserves, but when they join the euro not anymore.

Total reserves to GDP ratios for non-eurozone countries are more or less in line with eurozone countries. The Czech Republic has too much foreign exchange reserves, but these can be sold.

Knowing gold policy is shielded by secrecy laws, I decided to ask several central banks in the E.U. about their international reserves management. Perhaps one would spill the beans and reveal something about gold. My question:

Is there a legal requirement, or other agreement whatsoever, for countries in the European Union to hold a certain amount of international reserves (monetary gold and foreign exchange) relative to a country’s capital key in the European System of Central Banks, or relative to its GDP?

Without exception, the NCBs that replied wrote there are no agreements whatsoever. For example, from Romania:

Dear Sir,

In reply to your follow-up email of September 14th, 2022, concerning the existence of legal requirements regulating the amount of international reserves in relation to a country’s capital key in the European System of Central Banks, or to the country’s GDP, we would like to confirm that we are not aware of any such requirements.

Sincerely,

Public Information and Documentation Division

National Bank of Romania

Have a look at chart 9 again to see Romania’s total reserves versus GDP in comparison to the rest of the E.U. The parallels cannot be a coincidence.

From Germany, more of the same:

Advertisement

______________________________________________________

. . . there is no stuatutory obligation in Union law for NCBs to hold certain amounts of international reserves.

Additionally, I searched in the Treaty On The Functioning Of The European Union and The Statute Of The European System of Central Banks And Of The European Central Bank for clues. There is not a word on harmonizing reserves in these documents. Remarkable, given all the clear correlations.

Conclusion

It seems all countries in the E.U. have secretly agreed to the gold strategy I have outlined above. If my analysis is correct, and the trend of equalizing reserves continues, we can expect some countries in the E.U. to buy gold (i.e. the Czech Republic), others foreign exchange (i.e. Denmark), and still others sell foreign exchange (i.e. Croatia). Countries outside the E.U. will continue buying gold as well to come on par. Except, of course, the United States.

The reset described above will happen when all large economies are in an insurmountable crisis. Revaluing gold to cancel government debt is not something they want to do more often so it comes down to one window of opportunity. If one country goes at it alone prematurely it may spoil the opportunity of a smooth transition to a gold standard.

I don’t think European politicians and central bankers in the 1970s had a long term gold strategy that was written in stone. Things developed along the way. Views and decisions were probably shaped by central bankers at meetings at European clubs or the Bank for International Settlements. Some countries outside the E.U. play a comparable gold strategy. From the Swiss central bank (SNB):

The Swiss National Bank [SNB] completed its gold selling program of 1,300 tonnes on March 30, 2005. Before these sales, Switzerland’s relative position with respect to gold holdings was extreme among the G10 countries.

Europe aims to equalize gold to GDP ratios, not gold to monetary base ratios. As a consequence, the gold standard they envisage is more likely a system of gold price targeting rather than the classical gold standard. In the latter system people can exchange bank notes for gold at a fixed price at a (central) bank: the monetary base is backed by gold. With gold price targeting people can exchange gold in the free market at a price that is stabilized through central bank monetary policy.

The gold is evenly distributed in the eurozone, but the debt that needs to be cancelled is not. For example, Italy has a public debt to GDP ratio of 150%, while in Germany it’s 70%. Part 3 of this series will be about risk sharing: what options there are to transfer debt from Italy to other countries, in order to make most use of all NCBs’ revaluation accounts.

Source: Zero Hedge

Advertisement

______________________________________________________

______________________________________________________

If you wish to contact the author of a post, you can send us an email at voyagesoflight@gmail.com and we’ll forward your request to the author (if available). If you have any questions about a post or the website, you may also forward your questions and concerns to the same email address.

______________________________________________________

All articles, videos, and images posted on Dinar Chronicles were submitted by readers and/or handpicked by the site itself for informational and/or entertainment purposes.

Dinar Chronicles is an informational news aggregator. All content, including third-party reports and community commentary, is provided for educational purposes only. We do not provide financial, legal, or tax advice. We do not recommend the purchase or sale of any currency or investment. Please consult with a licensed professional before making any financial decisions.

Copyright © Dinar Chronicles

______________________________________________________

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}